I didn't see any mention of this Tony Hain paper:

http://tndh.net/~tony/ietf/ARIN-runout-projection.pdf

tl;dr: ARIN predicted to run out of IP space to allocate in August this year.

Are you ready?

I didn't see any mention of this Tony Hain paper:

http://tndh.net/~tony/ietf/ARIN-runout-projection.pdf

tl;dr: ARIN predicted to run out of IP space to allocate in August this year.

Are you ready?

In a message written on Tue, Apr 23, 2013 at 05:41:40PM -0400, Valdis Kletnieks wrote:

I didn't see any mention of this Tony Hain paper:

http://tndh.net/~tony/ietf/ARIN-runout-projection.pdf

tl;dr: ARIN predicted to run out of IP space to allocate in August this year.

Here's a Geoff Houston report from 2005:

https://www.arin.net/participate/meetings/reports/ARIN_XVI/PDF/wednesday/huston_ipv4_roundtable.pdf

I point to page 8, and the prediction "RIR Pool Exhaustion, 4 June

2013".

Those of us who paid attention are well prepared.

tl;dr: Real statistical models properly executed in 2005 were remarkably

close to the reality 8 years later.

I have sadly witnessed a growing number of businesses with /24s moving

to colocation/aws networks and not giving up their unused network

space. I assume this will come into play soon. I have already read the

news of blackmarket sales of network allocations in Europe.

Valdis Kletnieks <Valdis.Kletnieks@vt.edu> writes:

and I feel fine

I didn't see any mention of this Tony Hain paper:

http://tndh.net/~tony/ietf/ARIN-runout-projection.pdf

tl;dr: ARIN predicted to run out of IP space to allocate in August this

year.Are you ready?

Personally? Yes! Customer side? No! Well expect for some.

But at least here in Germany some companies (!= ISPs) noticed this IPv6

thing and now are looking for people to support them. Problem is: They

don't want to pay for it (e.g. less or equal to the usual hourly rate

or any other kind of project).

Two weeks ago:

"We need someone for a two day IPv6 workshop in two weeks!"

Yesterday:

"We need someone for a two day IPv6 workshop this week!"

Jens

I think what's very interesting for me is watching the consumer edge getting more IPv6 in north america.

It's important for everyone to talk to their vendors (now is a good day to call/write them) about what their IPv6-Only roadmap is. While folks may still have some IPv4-glue holding things together, getting that IPv6 to your customer and datacenter edge.

At minimum: It doesn't hurt to ask.

- Jared

On that note, something Mr. Huston wrote more recently:

"A Primer on IPv4, IPv6 and Transition"

http://www.potaroo.net/ispcol/2013-04/primer.html

Discussion:

https://news.ycombinator.com/item?id=5586519

this year.

I haven't seen discussion of how the policy of RIRs being able to

transfer space between themselves is going to affect the "end of the

world" numbers. Have I missed something?

And FWIW, Tony brought some of his early work on this topic to me when I

was at IANA in 2004, and even those initial projections were scarily

accurate.

Doug

Meanwhile, consumer-grade IPv6 still sucks, at "I have to turn off IPv6 to

watch YouTube videos" levels of suck...

The prediction of runout business is extremely hard. All of these predictions are based on the basic premise that what happened yesterday will most likely happen tomorrow. And in a world of very large populations this is highly likely - the larger the population its often the case that the smaller the impact of individual variations in behaviour. That means that once you get a very large population you'd expect a relatively low level of uncertainty in trend-based predictive models.

But the world of addresses is not so well behaved. For some years now we've seen the address world bifurcate into a small number of very large actors and a large number of much smaller actors. In the address world it was observed that less than 1% (its closer to around 0.5%) individual allocations account for more than half of the number of allocated addresses. This becomes a problem in the predictive models, as the dominant factor in address consumption is now the actions of some 20 or so very large entities. If they all fronted at the registry's front doors and asked for a three month allocation, and do so again in 90 days, and so on, then its pretty obvious that ARIN's remaining 40M addresses would not last more than one or two iterations of this cycle.

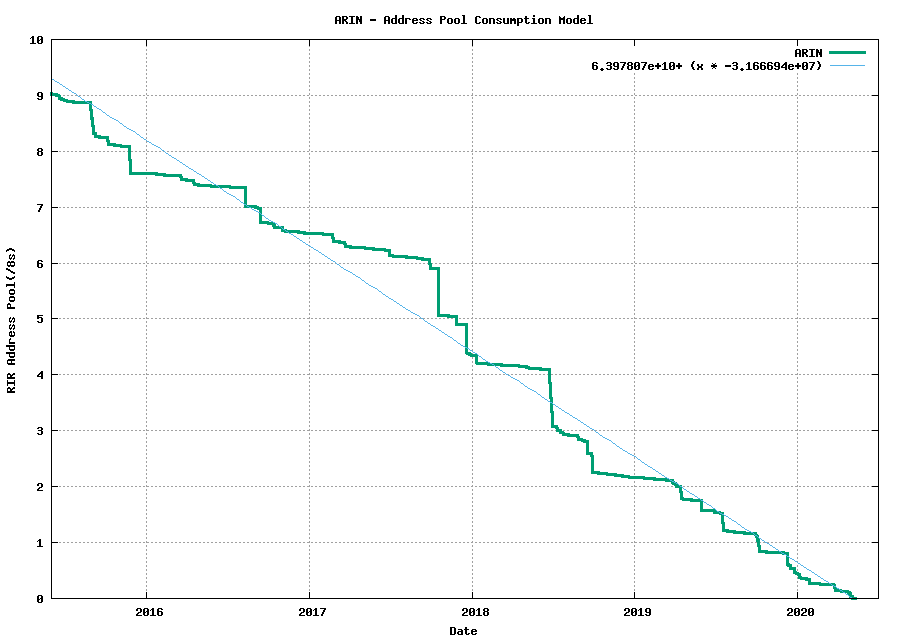

But what has been apparent in the ARIN region since the IANA runout of February 2011 has not been panic, but restraint. If you look at the run-down' of the address pool in ARIN over time (http://www.potaroo.net/tools/ipv4/arin-pool.png), you could certainly make the case that there was a pronounced run on address resources in ARIN in the last quarter of 2010, but it all changed in 2011. The ensuing 14 months following IANA runout, through 2011 and early 2012, saw a pronounced change in the region, and ARIN's address consumption in that period slowed down to a consumption rate that got as low as 1M addresses per month. This coincided in a change in the address allocation policy to reduce the time horizon of "demonstrated need" from 12 months to 3 months, but that factor alone would not account for the entirety of this slow down in the address consumption rates over this 14 month period.

Following a single largish allocation in early 2012 we've seen the ARIN address consumption rate increase somewhat, and the average rate of address consumption is currently around 2M addresses per month. If this rate of address consumption continues, the ARIN will reach its last /8 in early 2014, and if this rate persists, then the registry will exhaust its pool around the end of that year, or early 2015.

But given the uncertainty factors here as they relate to the distribution of large and small consumers in this area and changing sentiment about whether or not panic is a factor in address demands, I'd have to comment that the uncertainty factor of any prediction is high. Its quite plausible that exhaustion could occur some 6 - 9 months earlier than these dates.

However, personally I find it a little hard to place a high probability on Tony's projected exhaustion date of August this year. I also have to qualify that by noting that while I think that a runout of the remaining 40 M addresses within 4 months is improbable, its by no means impossible. If we saw a re-run of the address consumption rates that ARIN experienced in 2010, then it's not outside the bounds of plausibility that ARIN will be handing out its last address later this year.

thanks,

Geoff

I find it more entertaining that I recognized no less than three organizations

on that list that we've seen come up a lot recently in our spam scanning

systems.

Black market sales, handing out /15s to Romanian spammers like candy ..

Europe has had a lot of IP allocation fun

http://tndh.net/~tony/ietf/ARIN-runout-projection.pdf

tl;dr: ARIN predicted to run out of IP space to allocate in August this year.

http://www.potaroo.net/tools/ipv4/ says April 2014. That page worked well for the RIPE region.

I assume this will come into play soon. I have already read the news of blackmarket sales of network allocations in Europe.

It's not black market anymore, it's official. RIPE even has a web site where one can advertise that one wants to buy or sell.

* Andrew Latham

I have sadly witnessed a growing number of businesses with /24s

moving to colocation/aws networks and not giving up their unused

network space. I assume this will come into play soon.

A couple of /24s being returned wouldn't make a significant difference

when it comes to IPv4 depletion. Heck, not even a couple of /8s would.

Trying to reclaim and redistribute unused space would be a tremendous

waste of effort.

I have already read the news of blackmarket sales of network

allocations in Europe.

Interesting. Do you have a link or some other kind of reference?

Tore

<http://www.ripe.net/lir-services/resource-management/listing> is a "white market sales" place. Perhaps that's what the previous poster meant.

Searching for "IPv4 broker" yields a lot of results as well, that might be the "black market" though.

I also find it a bit strange that the runout in APNIC and RIPE was very different. APNIC address allocation rate accelerated at the end, whereas RIPE exhaustion date kept creeping forward in time instead of closer in time, giving me the impression that there wasn't any panic there.

Has anyone done any detailed analysis of the last year of allocation behaviour for each of these regions, trying to understand the difference in behaviour? I'd be very interested in this.

My belief (not well founded) is that ARIN runout will look more like RIPE region than APNIC...

One of the immediate results of RIPE NCC exhaustion was that ISPs

and colo now ask for monthly IPv4 space rental to end users, starting

with 1 EUR/IPv4 address per month, trend is up.

RIPE had shrinking allocation windows (12/9/6/3 months) and increasingly

strict scrutining of requests. Even in 3 months window period, people

showing need for >55k of IPs for that 3 months only got /17+/18 (48k)

instead of /16 one would expect - so in fact the windows were even

shorter in practise.

Geoff pointed out the large alloc players having a huge impact in the

end game scenario - this was effectively neutralized by this "soft

landing" policy, I'd say.

I'm not aware that APNIC also had such a "soft landing" policy in

effect, but I didn't monitor closely.

Best regards,

Daniel

I suspect that the extent of communication of expectations, the economic climate, the prevailing allocation window at the time (RIPE was working on 3 months whereas APNIC still had the 12 month window in place right up to the last /8) all play a part in such things.

The fast/slow nature of ARIN's address consumption profile over the last 30 months is certainly a new factor here - again there is likely to be some interplay between economics, the saturation of the wired market in that region, and the existing CGN deployments in some (much) of the mobile IPv4 space in North America which also give some credibility to a prediction of a more measured approach to exhaustion rather than a massive paniced run on what's left.

But then again APNIC and RIPE NCC both had last /8 policies in place, which has mitigated some of the impacts of address pool exhaustion. For smaller actors there is still a source of addresses in these regions, albeit a very limited trickle of addresses, but there is still some. As I understand it, ARIN will continue allocating right to the end of their IPv4 address pool and not hold back any addresses for this "last chance" trickle feed, or have I missed something crucial in ARIN's policy handbook?

Geoff

But then again APNIC and RIPE NCC both had last /8 policies in place, which has mitigated some of the impacts of address pool exhaustion. For smaller actors there is still a source of addresses in these regions, albeit a very limited trickle of addresses, but there is still some. As I understand it, ARIN will continue allocating right to the end of their IPv4 address pool and not hold back any addresses for this "last chance" trickle feed, or have I missed something crucial in ARIN's policy handbook?

Nope, you are correct Geoff. There is a /10 reserved for transition

technologies (e.g. outside addresses on a CGN) and there is a

"critical infrastructure" reserve, but no general purpose reserve like

in RIPE and APNIC.

~Chris

* Mikael Abrahamsson

I have already read the news of blackmarket sales of network

allocations in Europe.Interesting. Do you have a link or some other kind of reference?

<http://www.ripe.net/lir-services/resource-management/listing> is a

"white market sales" place. Perhaps that's what the previous poster meant.Searching for "IPv4 broker" yields a lot of results as well, that might

be the "black market" though.

"White market" transfers has been allowed in the RIPE region since late

2008, cf. http://www.ripe.net/ripe/policies/proposals/2007-08. There's

no requirement that the transferred space is put on the NCC's listing

service first - you can use a broker to arrange it if you want, or do it

completely in private.

For a transfer not to be "white", the transaction would need happen

without the NCC's knowing and blessing. This implies validations of the

receiver's operational need for the allocation, and updating the

registry/database to reflect the new holder. I'm genuinely interested in

reading articles or other research documenting that such "black market"

transfers are happening (or not).

Tore

{kind=link}